The great tax shift: How politicians promise tax cuts, then shift the costs onto you

Politicians make a lot of promises about taxes.

Ted Cruz claims:

As Washington pads Wall Street’s pockets, hard-working Americans get left behind. My tax plan will change that.

Donald Trump claims he’ll “make America great again” with his tax plan. Others have similar plans. Flat taxes, “fair” taxes, etc.

We’ve been hearing these same claims for 40 years. What actually happens is that politicians lower taxes, primarily for the wealthy, and then they do one of two things: 1) shift the costs onto you, or 2) run deficits.

When you hear pundits and politicians talk about taxes, forget what they say. The truth is simple: You’re going to pay more, and the wealthy are going to pay less.

As tax day approaches, here’s a story you won’t hear in the corporate media.

Donald Trump speaking at CPAC 2015 in Washington, DC (Gage Skidmore/CC-BY-SA 3.0)

All taxes are not created equal. Some benefit average people. Some benefit Wall Street and the wealthy.

Consumption taxes are taxes on goods and services that everyone buys regularly like food and gas. As you make more money, you don’t tend to buy more of these items. The wealthy pay very little in terms of consumption taxes. The costs are borne by consumers.

Progressive taxes, by comparison, are taxes where you pay more back as you benefit more. The idea behind progressive taxes is that the more people benefit from the efforts of our country, the more they should pay back in to help make sure we have strong infrastructure and a strong country and that future generations have the same opportunity to succeed.

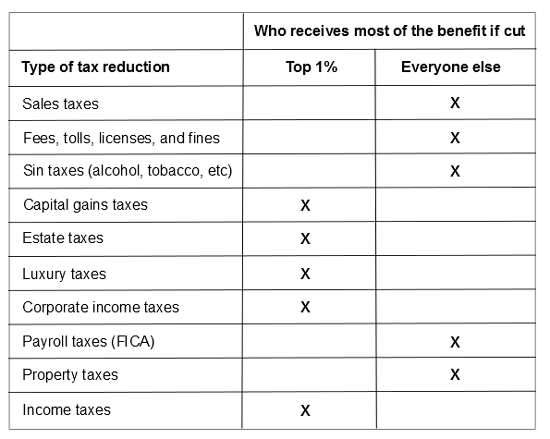

Here’s a list of 10 common taxes and who benefits most from reducing them.

Who receives the benefit when taxes are cut.

It’s fairly clear how most of these taxes are either progressive or regressive. Everyone buys food and everyday goods so sales taxes impact consumers. Wealthy people don’t typically buy any more food or consumer products than anyone else, so the bulk of sales taxes are collected from average people. Reducing sales taxes helps consumers and everyone equally. Similarlyfees, tolls, licenses, fines, and sin taxes are taxes that impact average people. Payroll taxes are paid by both employees and employers. However, the economic burden of payroll taxes falls on workers as the employers’ share of payroll taxes ispassed on to employees in the form of lower wages.

Capital gains taxes affect the profit on investment. Cuts to capital gains taxes primarily benefit people who can afford to invest and disproportionately benefit the wealthy who hold most of their wealth in stocks. Taxes on luxury items andestate taxes are taxes on wealth. If your “estate” is worth less than $5.43 million, you pay no federal tax.

Property taxes are a bit tricky. You might think property taxes affect only people who own property and also impact the wealthy more, as they own the most property. First, property taxes can be passed on to renters in the form of higher rent. Second, property owners have ways to reduce or offset the amount they pay in property taxes. For example, property owners receive an income tax deduction for interest paid on their homes. The more interest you’re paying, the bigger the tax deduction. There are also often loopholes that allow people to declare their property a farm or some other type of business for a tax deduction. Long story short—property taxes are usually paid by average people.

Corporate income taxes have to be paid by people since corporations are nothing more than pieces of paper. It’s often assumed that taxes on corporations are passed on to consumers; this is false. Prices are determined by supply and demand independently of tax rates. If this seems counterintuitive, ask yourself if you’ve ever seen a price go up or down because taxes were raised or lowered. This leaves two groups of people: Shareholders and employees. Most economists agree the costs of corporate taxes are borne by these two groups, though they disagree on the ratio. If you look at a number of estimates and average them, it’s close to 20 percent labor and 80 percent shareholders. The tax policy center methodology estimates this same 80/20 shareholder to labor split. Using this 80/20 split, corporate tax cuts would mostly benefit shareholders which means they will disproportionately benefit stockholders or the top 1 percent.

The United States and most states have a progressive income tax system. The idea is that as you make more and do better, you pay more back. For this reason, income taxes tend to be paid more by people who benefit more. This example, from Ohio’s 2015-16 proposed income tax changes, shows who would benefit most from income tax changes, the biggest being a 23 percent rate cut.

Who benefits from 2015 Ohio income tax changes (Policy Matters Ohio).

The top 1 percent would receive on average $13,096, while the next 4 percent would receive $1,395. Benefits drop off steeply for everyone else. Income tax cuts primarily benefit the wealthy.

Here’s how the tax shift works: Cut progressive taxes, raise consumption (regressive) taxes. In the wake of Ohio’s income tax cuts for the wealthy, the rest of Ohio is seeing property tax increases, sales tax increases, fee increases, sin tax increases, proposed tolls, etc.

The architects of the tax shift

In 1978, Jude Wanniski penned the article “A Bull Market Scenario” in the Wall Street Journal. The question he asked was:

What will it take to get the Dow Jones Industrial Average to a level of 3000 or 4000 by the early 1980s?

Wanniski believed the U.S. could recreate the conditions from 1921 to 1929 under Calvin Coolidge that led to a nearly five-fold rise in the stock market. Coolidge believed “generally speaking, the business of the American people is business” and lowered taxes to the point where in 1927, only the wealthiest 2 percent of taxpayers paid any federal income tax.

Wanniski’s idea was to duplicate the Coolidge plan:

As in the 1920’s, we can expect a gradual, then accelerating dismantling of the government barriers between effort and reward. An era of incentives. The most important of these barriers are the now unnecessarily high federal tax rates on capital gains, personal incomes, and gifts and estates. Also a diminution of federal regulatory barriers to commerce.

Sound familiar?

Wall Street street sign (Ramy Majouji/Creative Commons).

If you want the stock market to go up, the way to do this is to cut taxes on the wealthy and corporations (the capital gains tax, income taxes, corporate taxes, estate taxes, etc.). These taxes are taxes on accumulated wealth and capital. If you want to juice the stock market, eliminate taxes on accumulated wealth and capital.

Certain tax cuts benefit Wall Street and the wealthy.

Taxes that don’t fall into this category are the taxes paid by everyday people: Sales taxes, property taxes, sin taxes, government fees and tolls.

Look for these taxes to be raised.

Wanniski’s article became one of the cornerstones of supply-side economics under President Reagan. Cutting these taxes doesn’t boost the economy. It doesn’t boost demand. It doesn’t create jobs. It doesn’t help the middle class.

As Wanniski points out, these tax cuts benefit wealthy investors and juice the stock market.

What does this look like at the national level?

Let’s look at tax cut changes over the last 40 years.

In 1978, the Carter administration reduced the top tax rate on capital gains to 28 percent from 39 percent, reduced income taxes, increased the capital gains exclusion rate from 50 percent to 60 percent, and reduced the corporate tax rate from 48 percent to 46 percent.

Score: Top 1 percent — 4; Everybody Else — 0

Ronald Reagan gives a televised address from the Oval Office outlining his plan for tax reductions in July 1981 (White House Photo Office).

In 1981, Reagan passed the Economic Recovery Tax Act (ERTA). This included:

- Across-the-board income tax cuts. The top income tax rate dropped from 70 percent to 50 percent; the bottom rate dropped from 14 percent to 11 percent.

- Raising the estate tax exemption to $600,000.

These cuts were based on the idea that we could cut taxes and increase revenue through greater growth. Unfortunately, so much revenue was lost that Congress had to close several loopholes opened by the ERTA only a year later with the Tax Equity and Fiscal Responsibility Act (TEFRA) of 1982.

Score: Top 1 percent — 6; Everybody Else — 0

What we don’t often hear is that Social Security taxes were raised five times from 1977 to 1990. Social security taxes are the biggest tax paid by ordinary people, according to Reagan:

For the nation’s work force, the Social Security tax is already the biggest tax they pay. In 1935 we were told the tax would never be greater than 2% of the first $3,000 of earnings. It is presently 13.3% of the first $29,700, and the scheduled increases will take it to 15.3% of the first $60,600.

These tax increases on workers subsidized tax cuts for corporations and the wealthy, like the capital gains tax cuts and the estate tax cut.

Score: Top 1 percent — 11, Everybody Else — 0

In 1986, in the second of Reagan’s two major tax overhauls, the top tax rate for individuals was reduced from 50 percent to 28 percent, while the bottom rate was raised from 11 percent to 15 percent.

Score: 13-0

As a result of the trickle down tax cuts of the 1980s, revenue fell and the deficit rose. That led President George H.W. Bush to raise taxes in 1990 to try to keep the deficit in check.

Score: 13-1

In 1993, President Clinton raised the top two income tax rates slightly and raised the corporate tax rate by 1 percent (from 34 percent to 35 percent). However, he also increased the share of Social Security benefits that could be taxed and raised the sales tax on fuel (a consumption tax that affects consumers more than businesses).

Score: 15-3

In 1997, however, Clinton reduced the capital gains tax from 28 percent to 20 percent and raised the exemption on the estate tax to $1 million from $600,000.

Score: 17-3

George W. Bush accelerated the push in 2001 and 2003 with more tax cuts heavily favoring the wealthy. The exemption for the estate tax was raised to $5 million and the rate reduced. The Center on Budget and Policy Priorities estimates that 24.2 percent of tax savings from these changes went to the top 1 percent.

Score: 20-3

In 2010, the Bush tax cuts were up for renewal. President Obama fought to renew them for those earning less than $200,000 ($250,000 for joint filers). The U.S. Chamber vigorously fought leaving out those who earned more and eventually a compromise was reached where the original changes were extended for two years in exchange for some economic stimulus measures and a temporary one-year reduction in the payroll tax.

Score: 21-4

In 2012, the Bush tax cuts came up again. This time President Obama proposed making the tax cuts permanent for those with taxable incomes of $400,000 ($450,000 for joint filers) or less. For those above this level, the rate was increased from 35 percent to 39.6 percent and the capital gains tax was also raised from 15 percent to 20 percent. The payroll tax deduction from 2010 was eliminated.

Final Score: Top 1 percent — 22; Everybody Else — 6

Using this very simple method of scoring tax cuts, it’s pretty clear who receives most of the benefit of tax changes in America. This is largely the result of corporate special interest group lobbying by groups like the U.S. Chamber of Commerce, the largest special interest group in the country.

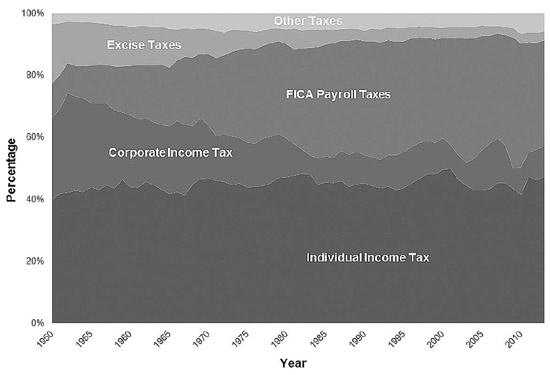

U.S. federal budget sources of revenue from 1950-2014 (Budget of the U.S. Government 2014, Historical Tables)

In 1952, corporate income taxes provided 32.1 percent of federal revenue. By 2013, corporate income taxes provided only 9.9 percent. In 1952, FICA payroll taxes provided 9.7 percent of federal revenue. In 2013, FICA payroll taxes provided 34.2 percent. Excise taxes including the estate tax provided 19.1 percent of federal revenue in 1952. By 2013, excise taxes provided only 5.5 percent of federal revenue.

If you score the tax changes at the national level using the table illustrating who they benefit, almost all of the tax changes have been designed to benefit the wealthy and Wall Street. Wanniski’s plan has come to fruition.

Not surprisingly, Wall Street is doing quite well, and average people are not. Benefits were supposed to trickle down—they didn’t. The rising tide lifted a few yachts but rolled right over everyone else.

An economy that works for everyone

National and state budgets and tax plans are not easy to decipher, especially since most of the business reporting in our country is just that, reporting done by our largest businesses. The report? We’re doing quite well thank you and we’d like to pay even less to states and the United States.

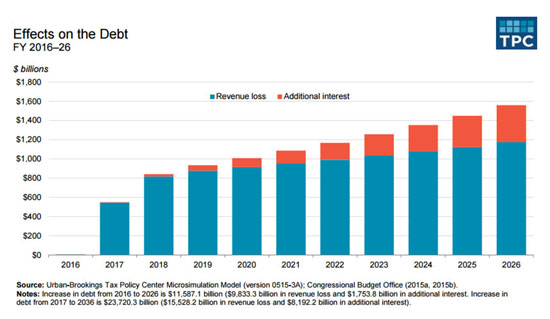

An analysis of Donald Trump’s plan by the Tax Policy Center reveals the rich would get a lot richer. His plan would reduce federal revenue by $9.5 trillion over the first decade and an additional $15 trillion in the next 10 years. It would cause the debt-to-GDP ratio to hit 180 percent by 2026. Ted Cruz’s plan isn’t much better. It would reduce federal revenue by $8.6 trillion in the first 10 years and we’d lose $12.2 trillion in revenue over the next 10 years.

Increases to national debt from proposed Trump tax plan (2017-2026) (Tax Policy Center).

These cuts will either be passed down to our kids in the form of debt, or raised by increasing taxes that benefit average people. The 99 percent will never see any benefit, just like we’ve seen no benefit from the past 40 years of tax shifting. All that’s happened is that loopholes were created for the wealthy and costs were shifted onto average people.

Ted Cruz has already proposed shifting the burden through a VAT tax. The VAT tax is a sales tax. It is regressive. Guess who would pay most of it? That’s right. The 99 percent.

We’re told that the 1 percent will invest and create more jobs. Anyone who’s taken even the most basic business courses knows that you hire people when there’s an increase in demand. Taking money from consumers (70 percent of GDP spending) reduces demand.

If we want to change this situation, we need to mobilize and vote for an economy that works for everyone—not just a few at the top).

David Akadjian is the author of The Little Book of Revolution: A Distributive Strategy for Democracy (now available as an ebook). Cross posted at Daily Kos.